Inflation – The Great Threat to Retirement

Just 18 months or so ago the headlines proclaimed mass unemployment. Today the news is of labour shortages and inflation.

But this is not a big surprise. The dramatic slump in activity in 2020 did not reflect underlying economic weakness but was a considered response to the Covid public health emergency.

As bottlenecks fade the immediate inflation surge should subside. Some underlying risk is likely to remain if demand in the economy remains strong, even as overall capacity grows.

The big central banks clearly signalled their willingness to let economies “run hot” for a while. Yet inflation may not be susceptible to fine tuning and there is a risk that today’s running hot becomes tomorrow’s overheating. In which case, monetary policy may yet end up tightening faster, and further, than central bankers and money markets expect.

Enemy No 1

The number one enemy of the long-term saver is inflation – the silent but steady increase of prices over time

The reason that we invest our money is to make it grow, ideally at a rate faster than inflation. When we measure investment returns, we should be measuring them relative to inflation. Say inflation is 3% and our investments grow by 7%, then we have achieved a ‘real return’ of 4%.

The inflation tax

If we view inflation as a tax, the mathematics make it clear that it is far more devastating than anything that has been enacted by HMRC.

The inflation tax has a powerful ability to consume capital.

It makes no difference to a saver earning 4% whether she pays 100% savings tax during a period of no inflation or pays no tax during a period of 4% inflation. Either way she is ‘taxed’ in a manner that leaves no real return in both scenarios.

She would likely be outraged at a 100% savings tax, but doesn’t notice that 4% inflation is the economic equivalent. They both leave her with no real return.

Eating into your retirement

In the twelve months to Jan 2022, inflation was 5.4% and the Bank of England expects inflation to continue rising, to around 6% by April 2022. This means that keeping money in cash is a good way to lose 5 – 6% per year.

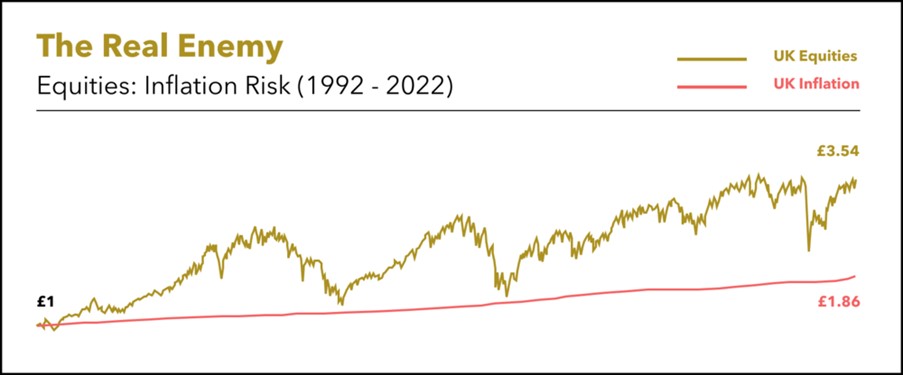

Over the last 30 years (about the length of an average two-person retirement), inflation in the UK has resulted in an item costing £1 in 1992 now costing £1.86 in 2022. This means your purchasing power has almost halved!

A solution

Throughout the same period £1 invested in the UK share market is worth c£3.50 today, and that’s ignoring 30 years of dividends. And this was during a three-decade period that included the dot-com bubble, the great financial crisis, and the Covid-19 pandemic.

And what did you have to do to earn this? Two things:

1. Invest and do nothing (harder than it sounds).

2. Do not panic when financial markets go through annual bouts of volatility

If you are concerned about protecting the real value of savings, please get in touch and we will be happy to assist.

Barra Gorman FPFS

Chartered Financial Planner

The purpose of this article is to provide technical and generic guidance and should not be interpreted as a personal recommendation or advice.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.